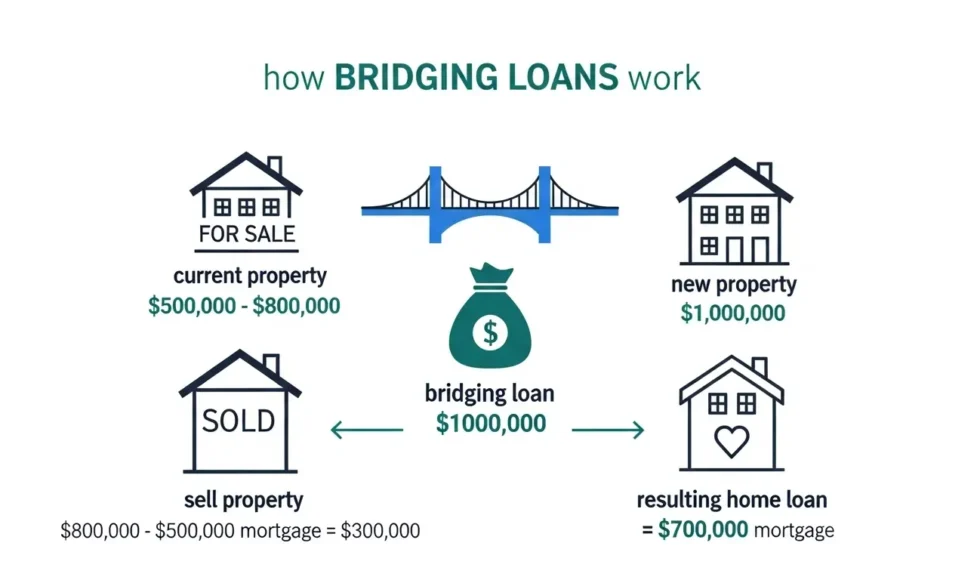

Bridge lending is often used when timing matters more than conventional financing speed. Whether the goal is to secure a property, close a time-sensitive transaction, refinance short-term debt, or move capital into a new opportunity, bridge loans are designed to provide fast, interim funding when traditional lending structures are too slow or too restrictive.

One of the most common questions borrowers ask before applying is simple: what credit score is needed for bridge lending?

The answer is not always as straightforward as it is with standard residential financing. Bridge lenders do look at credit, but in most cases, credit score is only one part of a broader lending decision. Asset value, exit strategy, borrower experience, equity position, and transaction strength often carry just as much, if not more, weight.

For borrowers and investors in Panama exploring short-term financing solutions, understanding how bridge lenders evaluate credit can help improve preparation and reduce financing friction.

This article explains what credit score is typically needed for bridge lending, what lenders actually look for, and how borrowers can position themselves more effectively.

Why Credit Score Matters in Bridge Lending

A credit score gives lenders a snapshot of how a borrower has managed debt and financial obligations over time. It helps indicate reliability, repayment behavior, and overall financial discipline.

In bridge lending, however, the role of credit is often more flexible than in conventional bank financing.

That is because bridge loans are generally structured around a short-term event, such as:

- Purchasing before a long-term refinance

- Closing on a commercial asset quickly

- Funding a value-add property strategy

- Covering a temporary capital gap

- Supporting a transitional business or asset-backed opportunity

Since these transactions are often time-sensitive and asset-driven, lenders may view the borrower through a wider risk lens rather than relying only on a credit score threshold.

Still, credit remains important because it can influence loan pricing, approval confidence, leverage, and the lender’s willingness to move forward.

What Credit Score Is Usually Needed for a Bridge Loan?

In most cases, bridge lenders prefer borrowers with a credit score of at least 620 to 680, although the exact requirement varies depending on the lender, the type of asset, the borrower’s profile, and the complexity of the transaction.

General Credit Score Ranges for Bridge Lending

Here is how lenders often interpret borrower credit:

700 and Above

This is generally considered strong for bridge lending. Borrowers in this range are often viewed more favorably, especially if the deal also includes a solid asset, clear exit strategy, and sufficient equity.

660 to 699

This range is often acceptable for many bridge lenders. Approval is still possible, particularly when the transaction is well-structured and the borrower has experience or a strong collateral position.

620 to 659

Many bridge lenders may still consider borrowers in this range, but they will usually pay closer attention to the full file. Loan terms may be tighter, and pricing may reflect higher perceived risk.

Below 620

Approval becomes more difficult, but not always impossible. Some lenders may still move forward if the property, equity, repayment strategy, and transaction quality are especially strong.

This is why borrowers often work with the best bridge loan lenders, rather than relying solely on conventional institutions. Experienced bridge lenders understand that not every strong opportunity fits neatly inside a traditional underwriting box.

Why Bridge Lenders Look Beyond Credit Score

Unlike long-term mortgage lenders, bridge lenders often focus more heavily on whether the deal makes sense and whether the borrower has a credible path to repayment.

That means a borrower with average credit may still qualify if the broader transaction is financially sound.

The Property or Asset Matters

In many bridge lending scenarios, the underlying asset is central to the lender’s decision. If the property has strong collateral value, clear resale potential, or refinance viability, it may offset moderate credit concerns.

This is especially relevant in commercial and transitional real estate financing, where short-term capital is often tied directly to asset repositioning or acquisition timing.

Exit Strategy Is Critical

Bridge loans are not designed to be held indefinitely. Lenders want to know exactly how the borrower plans to repay the loan.

A strong exit strategy might include:

- Sale of the property

- Refinance into long-term debt

- Incoming project capital

- Business liquidity event

- Stabilization followed by conventional financing

If the repayment path is realistic and well-supported, lenders may be more flexible on credit.

Borrower Experience Can Strengthen the File

Experienced borrowers often receive stronger consideration because they understand execution risk, timelines, and project management.

For example, an investor involved in joint venture real estate may not rely solely on personal credit if the project itself is well-structured, professionally managed, and backed by experienced partners. In these cases, lenders often underwrite the overall strength of the opportunity, not just the borrower’s score in isolation.

What Else Do Bridge Lenders Review?

A bridge lender typically evaluates several layers of risk before approving a loan. Credit score is only one of them.

Equity or Down Payment Position

The more equity a borrower has in the deal, the more protected the lender may feel. Lower leverage often improves approval odds and may help compensate for a weaker credit profile.

Debt History and Payment Behavior

Even if a borrower’s score is not ideal, lenders will often review why. A temporary issue from several years ago may be viewed differently than recent missed payments, defaults, or unresolved debt obligations.

Liquidity and Reserves

Lenders often want to see that the borrower has enough liquidity to handle interest payments, project expenses, or unexpected delays.

Documentation and Transaction Clarity

Bridge lenders move quickly, but they still expect a clear and organized file. Borrowers who present complete financials, project details, and repayment logic usually create stronger confidence.

Can You Get a Bridge Loan With Bad Credit?

Yes, in some cases, but it depends heavily on the strength of the transaction.

Borrowers with lower credit scores may still qualify if they have:

- Strong collateral

- Significant equity

- A clear and credible exit strategy

- Relevant project experience

- Additional guarantors or partners

However, lower credit often results in:

- Higher interest rates

- Lower loan-to-value ratios

- More lender scrutiny

- Additional documentation requirements

This is why choosing from the best bridge loan lenders matters. The right lender evaluates nuance and deal strength rather than rejecting a file based on a single score alone.

How Risk Protection Can Influence Bridge Loan Transactions

In more complex bridge transactions, lenders and borrowers may also evaluate legal and financial protections that reduce exposure during the loan term.

One example is personal indemnity insurance, which may become relevant in certain commercial or contractual contexts where personal guarantees, legal obligations, or transactional liability are involved.

While this type of protection is not a standard requirement in every bridge loan, it reflects a broader principle in short-term lending: sophisticated deals are often supported by layered risk management, not just borrower credit alone.

For borrowers entering higher-value or partnership-based transactions, understanding these protections can be important.

Bridge Lending in Investor and Capital-Structured Deals

Bridge lending is not limited to simple acquisition scenarios. It is often used in broader investment and project structures where timing, capital layering, and transaction execution all matter.

For example, a borrower or sponsor working alongside a venture capital investment fund may use bridge financing to secure a property, close a strategic asset, or fund a transitional phase before larger capital is deployed.

Similarly, in certain real estate or acquisition scenarios, borrowers may need short-term support for earnest money obligations or acquisition commitments. This is where emd funding can become relevant, particularly in competitive transactions where timing and proof of capital are critical.

In these situations, lenders often assess the overall capital stack, transaction credibility, and sponsor capacity alongside borrower credit.

That means bridge lending is often as much about structure as it is about score.

How to Improve Your Chances of Approval

If you are considering bridge financing, there are several practical steps that can strengthen your position before applying.

Strengthen the Transaction Narrative

Bridge lenders want clarity. Be prepared to explain what the loan is for, how long it is needed, and how it will be repaid.

Improve Credit Where Possible

If your score is just below a preferred threshold, paying down revolving balances, resolving recent delinquencies, or correcting reporting errors can help improve lender perception.

Bring Organized Documentation

A clean and well-prepared file creates confidence and often speeds up review. This includes:

- Asset details

- Purchase or transaction documents

- Financial statements

- Exit strategy explanation

- Relevant borrower or sponsor background

Work With the Right Lending Source

Not every lender is built for bridge transactions. Working with the best bridge loan lenders improves the likelihood of finding a structure that matches the actual deal rather than forcing the deal into an unsuitable lending model.

What Borrowers in Panama Should Keep in Mind

In Panama, bridge lending can be especially relevant for commercial property transitions, development timing gaps, investor-led acquisitions, and short-term strategic financing needs. But speed should never replace structure.

Borrowers should evaluate:

- Whether the lender understands asset-backed and transitional financing

- How repayment is expected to occur

- Whether the pricing aligns with the actual risk

- What documentation and legal protections are required

- How the financing fits into the broader investment objective

Bridge lending can be highly effective when used correctly, but it works best when the borrower enters the transaction with a realistic plan and professional guidance.

Conclusion

So, what credit score is needed for bridge lending? In most cases, a score between 620 and 680 is a common starting point, with stronger terms often available to borrowers above that range. However, bridge lenders typically look beyond credit score and evaluate the full strength of the transaction.

Collateral, equity, repayment strategy, borrower experience, and deal structure often matter just as much as the number itself.