A credit card limit enhancement is a process where your issuer increases the maximum amount you can borrow on your card. It gives you more buying power and can improve your credit utilization ratio when managed well.

According to recent data from the Federal Reserve, the average credit card limit in Latin America increased by 12% in 2023. For cardholders in Panama, understanding how to request and qualify for a higher limit can unlock better financial flexibility and strengthen your creditworthiness.

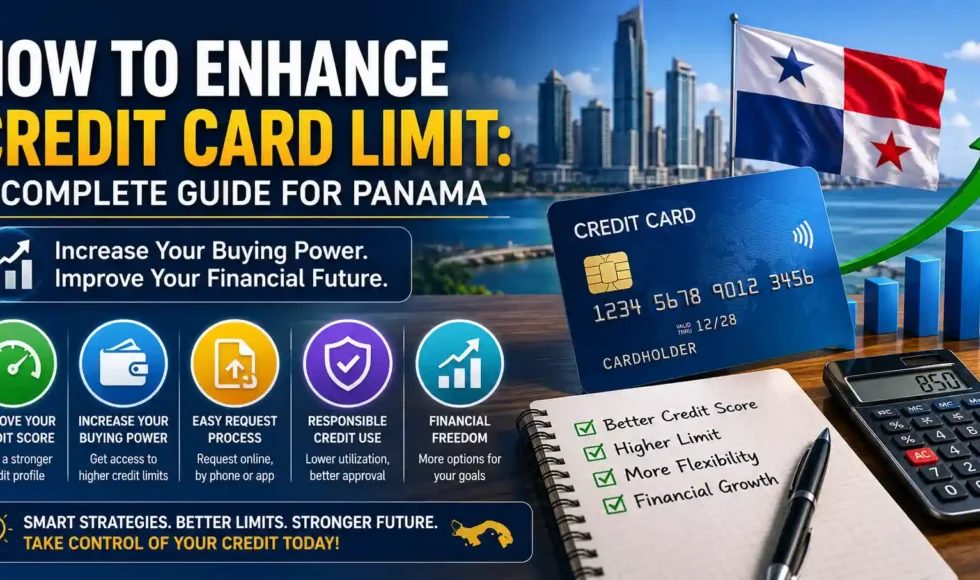

This guide walks you through proven methods to boost your credit limit, what lenders look for during reviews, and how services like credit enhancement solutions can support your financial goals.

What Is Credit Enhancement and Why Does It Matter?

Credit enhancement refers to strategies that improve your creditworthiness or reduce risk for lenders, making you eligible for higher credit limits or better loan terms. It can involve improving your credit score, increasing income documentation, or using third-party guarantees.

When you apply for a credit limit increase, banks review your financial profile. They want proof you can handle more credit responsibly. Credit enhancement techniques make your application stronger.

For businesses in Panama seeking capital solutions, a project investment partner can provide structured financing that complements personal credit strategies.

Types of Credit Enhancement

Credit enhancement comes in several forms. Personal credit enhancement focuses on improving your credit score and payment history. Corporate credit enhancement involves collateral, guarantees, or insurance products.

- Internal enhancement: Overcollateralization or reserve accounts

- External enhancement: Third-party guarantees from an indemnity insurance company

- Structural enhancement: Subordination or cash flow prioritization

Each type serves different financial goals. Personal cardholders typically focus on score improvement. Business owners might explore commercial insurance company products that protect against default risk.

How Can You Request a Credit Limit Enhancement Successfully?

You can request a credit limit increase by contacting your card issuer directly through their customer service line, mobile app, or online portal, and providing updated income information and credit history. Most banks review your account activity, payment patterns, and current credit score before approving the request.

Timing matters. Wait at least six months after opening your account or receiving your last increase. Banks prefer to see consistent payment history before granting additional credit.

Steps to Request Your Increase

- Check your credit score and fix any errors on your report

- Update your income information with your issuer

- Confirm whether the request triggers a hard credit inquiry

- Submit your request through the issuer’s preferred channel

- Provide documentation if the issuer asks for proof of income

Some issuers offer automatic increases based on account performance. If you consistently pay on time and keep balances low, you might receive an increase without asking.

What Factors Do Issuers Consider for Credit Limit Increases?

Card issuers evaluate your credit score, payment history, income level, debt-to-income ratio, and account age when reviewing credit limit enhancement requests. They want assurance you can manage additional credit without defaulting.

Your credit utilization ratio plays a huge role. If you regularly max out your current limit, issuers might hesitate to give you more. Keeping utilization below 30% signals responsible credit management.

| Factor | What Issuers Look For | Impact on Approval |

| Credit Score | 700 or higher preferred | High |

| Payment History | No late payments in 12 months | Very High |

| Income Level | Sufficient to cover new limit | High |

| Account Age | At least 6 months old | Medium |

| Current Utilization | Below 30% consistently | High |

Banks also review your recent credit inquiries. Too many hard pulls in a short period suggest you’re desperate for credit, which raises red flags.

How Does Credit Utilization Affect Your Limit Enhancement Chances?

Credit utilization measures how much of your available credit you’re using, and keeping it below 30% demonstrates financial discipline that makes issuers more likely to approve limit increases. Lower utilization shows you don’t depend heavily on borrowed money.

If your current limit is $5,000 and you carry a $4,500 balance, you’re using 90%. That signals risk. Paying down to $1,500 drops utilization to 30%, making you a better candidate for enhancement.

Calculating Your Utilization Rate

Add up all your credit card balances. Divide by your total available credit across all cards. Multiply by 100 for the percentage.

Example: $3,000 in balances divided by $15,000 in total limits equals 0.20, or 20% utilization. That puts you in good standing for requesting increases.

What Should You Do If Your Credit Limit Enhancement Request Gets Denied?

If denied, review the rejection reason, pay down existing balances, wait three to six months, and work on improving your credit score before reapplying. Issuers must provide an explanation for denial, which guides your next steps.

Common denial reasons include recent late payments, too many credit inquiries, or insufficient income. Address the specific issue before trying again.

Alternative Options After Denial

Consider applying for a new credit card instead. A new account adds to your total available credit, which improves utilization even without increasing your existing limit.

Business owners facing credit challenges can explore commercial bridge loan options for short-term capital needs. These loans provide liquidity without relying solely on personal credit cards.

Another option involves emd transactional funding for real estate investors who need quick access to earnest money deposits without tying up personal credit lines.

How Can You Build Credit to Qualify for Higher Limits?

Building credit takes time but follows predictable patterns. Pay every bill on time. Keep balances low. Avoid opening too many accounts at once.

- Set up automatic payments to never miss due dates

- Request higher limits on existing cards after 6-12 months of good behavior

- Become an authorized user on someone else’s well-managed account

- Dispute any errors on your credit report immediately

- Keep old accounts open to maintain longer credit history

Credit scores above 750 typically qualify for the best limit increase offers. Getting there requires consistent habits over months, not quick fixes.

Frequently Asked Questions

How long should I wait before requesting a credit limit increase?

Wait at least six months after opening your account or receiving your last increase. Banks prefer to see consistent payment history before granting additional credit. Some issuers have specific waiting periods, so check your terms.

Does requesting a credit limit increase hurt my credit score?

It depends on whether the issuer performs a hard inquiry. Soft inquiries don’t affect your score, but hard pulls can lower it by a few points temporarily. Always ask before submitting your request.

Can I request increases on multiple credit cards at once?

You can, but multiple hard inquiries in a short period might hurt your credit score. Space out requests by several months unless the issuer uses soft pulls for existing customers.

What income level do I need to qualify for a credit limit increase?

There’s no universal threshold, but your income should comfortably cover your current debt obligations plus the new credit limit. Issuers typically want debt-to-income ratios below 40%.

Will paying off my balance immediately after a purchase help my utilization?

Yes, but timing matters. Pay before your statement closing date so the lower balance gets reported to credit bureaus. Paying after the statement closes but before the due date still avoids interest but reports higher utilization.

Can business credit products help with personal credit limit goals?

Not directly, but business credit lines separate business expenses from personal cards, reducing your personal utilization. This can indirectly improve your personal credit profile and make you more attractive for limit increases.

What happens if I get denied for a credit limit increase?

The issuer must provide a reason for denial. Use that feedback to address specific issues like late payments or high utilization. Wait three to six months, make improvements, and reapply or consider a new card application instead.